Harvey Insurance Ltd. Blog

|

You hear the sound of crunching metal, your heart is racing, your palms are sweating— you’ve just been in an accident.

0 Comments

The backyard skating rink is a beloved tradition for families across the country. It calls to mind memories of lacing up skates on chilly winter nights, shooting the puck around with friends, then sipping hot cocoa and snuggling up by a crackling fire. If you’re tempted to bring back your childhood in the form of a DIY ice rink, it’s important to understand what is and isn’t covered under your home insurance policy and take the right measures to protect yourself in case anything goes wrong. Building a skating rink in your yard is a liability risk. Like a swimming pool, a skating rink increases the chances of someone getting injured on your property or causing damage to a neighbour’s property. What if someone slips and breaks a leg? What if your kid accidentally shoots a puck through your neighbour’s window? Or what if your rink floods your neighbour’s yard when it melts in the spring? Even if someone gets hurt after sneaking into your yard for a late-night skate, you could still be considered responsible. This is why it’s so important to make sure you have enough third-party liability coverage on your home insurance policy to protect you if you’re held liable for an injury or property damage. If you’re planning on building a skating rink on your property, ask your home insurance broker if your existing coverage is enough, or if they recommend increasing your liability limit for this new risk.

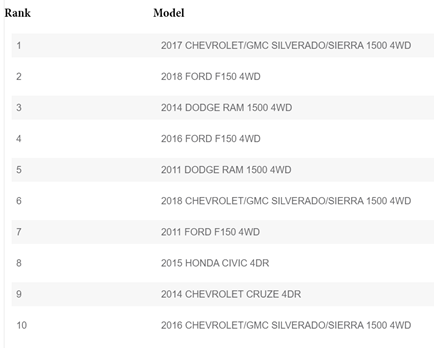

According to the Insurance Bureau of Canada, auto theft costs Canadians close to $1 billion each year. These vehicles were at the top of car thieves’ shopping lists in 2020:  Was your vehicle at the top of car thieves’ shopping lists in 2020? Find out now and take some simple steps to avoid being an easy target for vehicle theft.

|

Contact Us

(506) 366-2022 Archives

April 2021

Categories |

RSS Feed

RSS Feed